Turkey — Comprehensive Analysis: Economy, Geopolitics and Kabbalah

Turquía — Análisis Integral: Economía, Geopolítica y Cábala

טורקיה — ניתוח מקיף: כלכלה, גיאופוליטיקה וקבלה

"Gevurah is not punishment — it is the necessary limit that creates the vessel for what comes after."

— Kabbalistic principle of restriction and form

Executive Summary

Turkey is at this moment one of the most kabbalistcally active nations in the world. On the economic plane, it is traversing a genuine disinflation cycle — inflation fell from its peak of 85% to 30.87% in March 2026 — but the energy shock from the US-Israel-Iran war has interrupted its trajectory, pushing Brent above $118/barrel at the March peak. On the political plane, Erdoğan consolidates institutional power while the polls turn against him: opposition figure İmamoğlu is a presidential candidate from prison. On the geopolitical plane, Turkey emerges as the indispensable energy and diplomatic hub — TurkStream is the only active Russian pipeline to Europe, the Kirkuk-Ceyhan pipeline reactivated in March 2026 runs 1,600 km to the Mediterranean, and Ankara hosts the NATO summit in July 2026. And on the kabbalistic plane, everything converges: the year 5786 in the Hebrew calendar coincides with the numerical value of the Arabic Bismillah (786), USD/TRY has already passed through the level 38 = Galah (Exile/Revelation), the Lira in Hebrew is Ram (Exalted = 240), and the 6th Chai cycle since the founding of the Republic points to 2031 as the next major inflection point.

The synthesis is this: Turkey is living a Gevurah contraction — restrictive, dense, apparently descending. But Gevurah has a purpose that Chesed cannot fulfill: to create the vessel. The fall of the Lira is a Tzimtzum — the contraction that precedes expansion. The investor who understands this does not read USD/TRY as a thermometer of failure, but as a map of a spiritual process in progress.

I. Economic Situation

Inflation and interest rates

Turkey's disinflation campaign is one of the most significant adjustments of any emerging market in the last three years. The Central Bank of the Republic of Turkey (TCMB) raised the policy rate from 8.5% in mid-2023 to a maximum of 50% at the 2024 peak, precipitating an inflation decline of ~75 percentage points in less than two years.

| Period | CPI (Year-on-Year %) | Core CPI | Monthly Change |

|---|---|---|---|

| Peak (May 2024) | ~85% | 75.81% | — |

| Sep. 2024 | 49.4% | — | — |

| Dec. 2024 | 44.4% | — | — |

| Dec. 2025 | 30.9% | — | — |

| Jan. 2026 | 30.65% | — | +4.84% |

| Feb. 2026 | 31.53% | 29.46% | +2.96% |

| Mar. 2026 | 30.87% | 29.68% | +1.94% |

Source: Trading Economics – Turkey Inflation | Trading Economics – Core Inflation

The March 2026 reading came in below market expectations (31.4%), indicating that the pass-through of the oil shock to prices has been more contained than expected. The independent group ENAG places the real rate at 54.62% annually — above the official TÜİK figure — reflecting persistent methodological disputes over basket composition. Even so, the trend from the peak is unambiguous.

The TCMB rate-cutting cycle has been paused, not cancelled. After cutting 1,300 basis points from the peak over roughly six months, the Monetary Policy Committee held the rate at 37% on March 12, 2026, citing geopolitical uncertainty from the Middle East conflict. BBVA Research projects the rate at 32% by end-2026, with upside risks given energy pressures.

| Meeting | Policy Rate | Change |

|---|---|---|

| Peak (2024) | 50.00% | — |

| Dec. 2025 | 38.00% | −200 bps |

| Jan. 22, 2026 | 37.00% | −100 bps |

| Mar. 12, 2026 | 37.00% | No change |

| Apr. 22, 2026 | 37.00% | Pause expected |

The overnight reference interest rate band is 35.50% (lending) / 40.00% (deposit). The medium-term inflation target remains at 5% — a path that still requires years of discipline.

GDP and growth

Turkey grew 3.6% in 2025, driven by private consumption (+4.7 percentage points of contribution). GDP in dollars reached $1.59 trillion, with GDP per capita of $18,040 versus $15,325 in 2024 — a jump of nearly $3,000 per person in one year, reflecting the nominal stabilization of the lira. The World Bank revised its 2026 forecast downward from 3.7% to 2.8% on April 8, citing higher energy and food prices resulting from the regional conflict.

| Institution | 2026 Forecast | 2027 Forecast | Notes |

|---|---|---|---|

| IMF (Feb. 2026) | 4.2% | 4.1% | Pre-conflict |

| World Bank (Jan. 2026) | 3.7% | 4.4% | Pre-conflict |

| World Bank (Apr. 8, 2026) | 2.8% | 3.7% | Revised downward |

| BBVA Research | 4.0% | — | Downside risks |

| BNP Paribas | 3.8% | 4.0% | Less imbalanced growth |

| Government MTP | 3.8% | 4.3% | Official target |

Sources: IMF Article IV | Garanti BBVA Activity Pulse

Current account and energy dependence

The current account deficit more than doubled from 2024 to 2025: from $10.2 billion to $25.2 billion, reflecting an energy bill exceeding $65 billion annually. The gap on a rolling 12-month basis reached $32.9 billion (2.2% of GDP) in January 2026, up from just 0.8% of GDP in 2024.

The vulnerability is structural: Turkey is 100% dependent on imported oil and covers 85-90% of natural gas with imports. Each $10 increase in Brent adds $4.5-5.0 billion to the current account deficit, according to the Turkish Treasury. At the peak of the March 2026 shock, with Brent above $118/barrel versus the $70 baseline scenario, the annualized incremental impact exceeds $22 billion — enough to push the deficit toward 3% of GDP if sustained.

Tourism acts as an essential counterweight: 2025 tourism revenues reached a record $65.2 billion (+6.8% year-on-year), with 63.9 million visitors. The services balance finances almost the entire energy bill in normal years — this equilibrium is Turkey's main differentiating factor versus other emerging markets equally vulnerable to oil.

Reserves and external debt

TCMB gross reserves reached an all-time high of $218.2 billion on January 30, 2026, then fell to $161.6 billion on April 3 following massive intervention linked to the Middle East conflict shock. The central bank sold more than $38.5 billion in foreign exchange between mid-February and end-March. Net reserves (excluding swaps) collapsed from $78.6 billion to ~$24 billion in that period — the sharpest relative decline since the 2023 crisis.

Gross external debt reached $547.7 billion in Q2 2025 — a nominal record but equivalent to only ~34.5% of GDP, down from 48.7% in 2022. 53% of central government debt is denominated in foreign currency, implying direct sensitivity to lira depreciation. BNP Paribas projects external debt at 34.7% of GDP for 2026.

Banking sector

The Turkish banking system maintains a solid capital position — capital adequacy ratio of 18.2% in July 2025 — but shows visible deterioration in asset quality. The non-performing loan (NPL) ratio rose from 1.7% in mid-2024 to 2.59% in February 2026, concentrated in credit cards and SMEs. Total banking system assets reached 48.87 trillion liras in February 2026.

Deposit dollarization stabilized at around 40% — the KKM program (exchange-rate-protected deposits) was wound down in August 2025 after a total cost to the government estimated at $60 billion. Lira-denominated deposits now represent 60.7% of the total — up from 37% in 2023 — a sign that "liraization" has real momentum.

Credit ratings

The ratings upgrade cycle that began in 2024 has encountered its first setback. Fitch, which had raised the outlook to Positive in January 2026, lowered it back to Stable in April 2026 due to reserve losses during the geopolitical crisis. S&P has scheduled a review for April 17, 2026 that markets will watch closely.

| Agency | Rating | Outlook | Last action | Notes |

|---|---|---|---|---|

| Moody's | Ba3 | Stable | Jul. 2025 | Upgrade from B3 (Jan. 2024) |

| S&P | BB- | Stable | Apr. 2025 | Review: Apr. 17, 2026 |

| Fitch | BB- | Stable | Apr. 2026 | Positive outlook downgraded |

| Scope | BB- | Stable | Oct. 2025 | — |

Source: TheGlobalEconomy – Turkey Ratings

All four agencies place Turkey 3 notches below investment grade. The return to investment grade — which would catalyze massive passive capital flows — requires a rating of at least BBB-, which in the most optimistic scenario would not occur before 2027-2028.

II. Political Situation

Erdoğan: consolidated but eroded power

After 23 years in power, Erdoğan enters 2026 in a structurally secure but politically eroded position, with signs of physical decline that have opened the succession debate explicitly for the first time. His current mandate extends to May 2028. Under current rules, he cannot seek a third term — unless a constitutional reform is approved (which would require 360 votes out of 600 in parliament) or early elections are called that reset the term counter. The AKP began internal "self-criticism sessions" in January 2026 — a sign of the accumulated electoral pressure.

The polls are unambiguous: the CHP leads the AKP by 3.1-3.5 percentage points in voting intentions. In direct presidential duels, Ankara mayor Mansur Yavaş surpasses Erdoğan 58.6% to 41.4%. 67.1% of Turks believe that economic recovery requires a change of government — including 40% of the AKP-MHP base.

İmamoğlu: presidential candidate from prison

On March 19, 2025, Ekrem İmamoğlu was detained and transferred to Marmara prison. The charges include corruption, bribery, money laundering, and alleged support for the PKK. The day before, Istanbul University annulled his academic degree — required to run for president under the Constitution. Despite all this, 14.85 million CHP members voted for him in the primaries and the party officially nominated him as presidential candidate. The prosecutor is seeking a sentence exceeding 2,000 years in prison. İmamoğlu declared from prison: "The government escalates pressure and hostility against us as its defeat approaches."

The arrest triggered the largest protests in Turkey since Gezi Park in 2013: the lira fell 12.7% to 42 liras per dollar, the Borsa Istanbul plunged 8.72%, and roughly $16 billion exited the market. The TCMB spent $25 billion in reserves to stabilize the currency.

AKP succession: four candidates, no certainty

The succession race within the AKP has crystallized around four figures, with none of them having a guaranteed path:

- Hakan Fidan (Foreign Minister): considered the most capable on paper by analysts at The Economist, but with tense relations with intelligence chief Ibrahim Kalın.

- Selçuk Bayraktar (drone magnate, Erdoğan's son-in-law): symbol of Turkish defense power, with no electoral track record.

- Süleyman Soylu (former Interior Minister): 32.5% preference in internal AKP polls; polarizing outside the base.

- Bilal Erdoğan (the president's son): 87.5% of respondents say they would "definitely not vote" for the AKP if he were leader.

The Austrian Institute for International Affairs warns that the succession crisis is accelerating autocratization — the restriction of democratic freedoms is the mechanism for controlling transitional uncertainty. Turkey ranks 159 out of 180 in the RSF Press Freedom Index, with more than 515 journalists prosecuted in the first half of 2024.

III. Geopolitical Position

NATO and the Ankara Summit 2026

Ankara will host the NATO summit in July 2026 — this is not a protocol detail but what the Atlantic Council describes as a "strategic framing opportunity" that could improve predictability in the US-Turkey relationship. Relations with Washington, under the Trump 2.0 administration, have shifted from "crisis management" to "pragmatic cooperation." The most concrete point: the S-400 systems acquired from Russia have remained undeployed since 2019, and US Ambassador Tom Barrack stated in December 2025 that Turkey was "ready to return the S-400s to Russia" to rejoin the F-35 program, with a 4-6 month timeline.

However, the US-Israel-Iran war complicated the relationship: Turkey denied US forces access to its airspace, land, and maritime territory for operations against Iran on February 28, 2026, and rejected logistical cooperation. Ankara framed this as its mediator role. The July 2026 summit will be the stage where this tension is processed institutionally.

Turkey-Russia: TurkStream, the only active Russian pipeline in Europe

Since January 1, 2025, when the Ukrainian transit agreement expired, TurkStream became the only active pipeline carrying Russian gas to Europe. Flows in March 2026 increased 22% year-on-year to 55 million cubic meters per day, according to Anadolu Agency. Russia supplies 35-42% of Turkey's imported gas, and the Akkuyu nuclear plant (4 reactors of 1,200 MW each, operated by Rosatom with $9 billion in additional financing in December 2025) is expected to generate its first electricity in 2026.

A complicating factor is EU Regulation 2026/261 of January 2026, which establishes a legally binding ban on imports of Russian pipeline gas by September 30, 2027. The regulation specifically targets the Strandzha 1 interconnection point (TurkStream's entry into Europe via Bulgaria), which directly undermines Turkey's ambitions to be a re-exporter of Russian gas.

Turkey-Iran: "active neutrality"

On February 28, 2026, US and Israeli military strikes against Iran — which killed Supreme Leader Khamenei — presented Turkey with the sharpest geopolitical test of the Erdoğan era. The response: Erdoğan condemned both the attack and the Iranian retaliation, denied logistical access to US forces, and positioned himself as the only actor in contact with both Washington and Tehran. Foreign Minister Fidan proposed the "Istanbul Process" and the "Board of Peace" as mediation frameworks. A ceasefire was reached in early April 2026. Turkey, whose NATO membership with the alliance's second-largest army protected it from direct Iranian attacks, demonstrated that diplomacy can function as a strategic shield.

Hormuz and the Kirkuk-Ceyhan pipeline

The disruption of the Strait of Hormuz — through which ~20% of the world's oil supply transits — pushed Brent from $70 to $118/barrel. Tanker traffic on the most tense days fell to nearly zero. In this context, Turkey emerged as a substitute corridor: the Kirkuk-Ceyhan pipeline (capacity of 1.5 million barrels/day) was reactivated on March 17, 2026 after 12 years of inactivity. Initial flows of 170,000 barrels/day are expected to grow to 250,000 barrels/day, carrying crude from northern Iraq to the Mediterranean. Energy Minister Bayraktar also raised the possibility of a gas pipeline from Qatar to Europe via Turkey, relevant if LNG infrastructure suffers damage.

Turkey-Israel: total rupture

In August 2025, Turkey formally severed all commercial and economic ties with Israel, closed its airspace to Israeli aircraft, and banned maritime traffic to Israeli ports. The $7 billion annual bilateral trade was suspended. In February 2026, Turkey stopped issuing EUR-MED certificates for exports to Israel, closing a key alternative route. Israel today designates Turkey as a "rival"; former Prime Minister Naftali Bennett called it a "new threat." The two countries compete directly in Syria.

Turkey-Pakistan: emerging strategic alliance

The Turkey-Pakistan alliance has deepened to an unprecedented structural level. Erdoğan visited Pakistan in February 2025; 24 MoUs were signed covering air force, electronic warfare, and defense production. A permanent Joint Defense, Intelligence and Security Committee was established. On April 7, 2026, Pakistan and Turkey renewed their commitment to strengthening military cooperation with emphasis on joint training and exercises. Analysts describe the relationship as the construction of an "eastern multilateral alternative" that reduces dependence on the West.

Syria: Erdoğan's greatest strategic victory

The collapse of the Assad regime in December 2024 was the defining geopolitical event for Turkey of this generation. Turkey went from fighting a threat on its southern flank to being the dominant external power in Syria. The PKK formally announced its dissolution on May 12, 2025, following the ceasefire call by its imprisoned leader Abdullah Öcalan. Turkey completed a natural gas pipeline from Kilis (Turkey) to Aleppo in May 2025, integrating Syria into its energy corridor ambitions. Defense Minister Güler confirmed in February 2026 that Turkish troops will not withdraw from their bases in Syria or northern Iraq until Turkey considers its security objectives fulfilled.

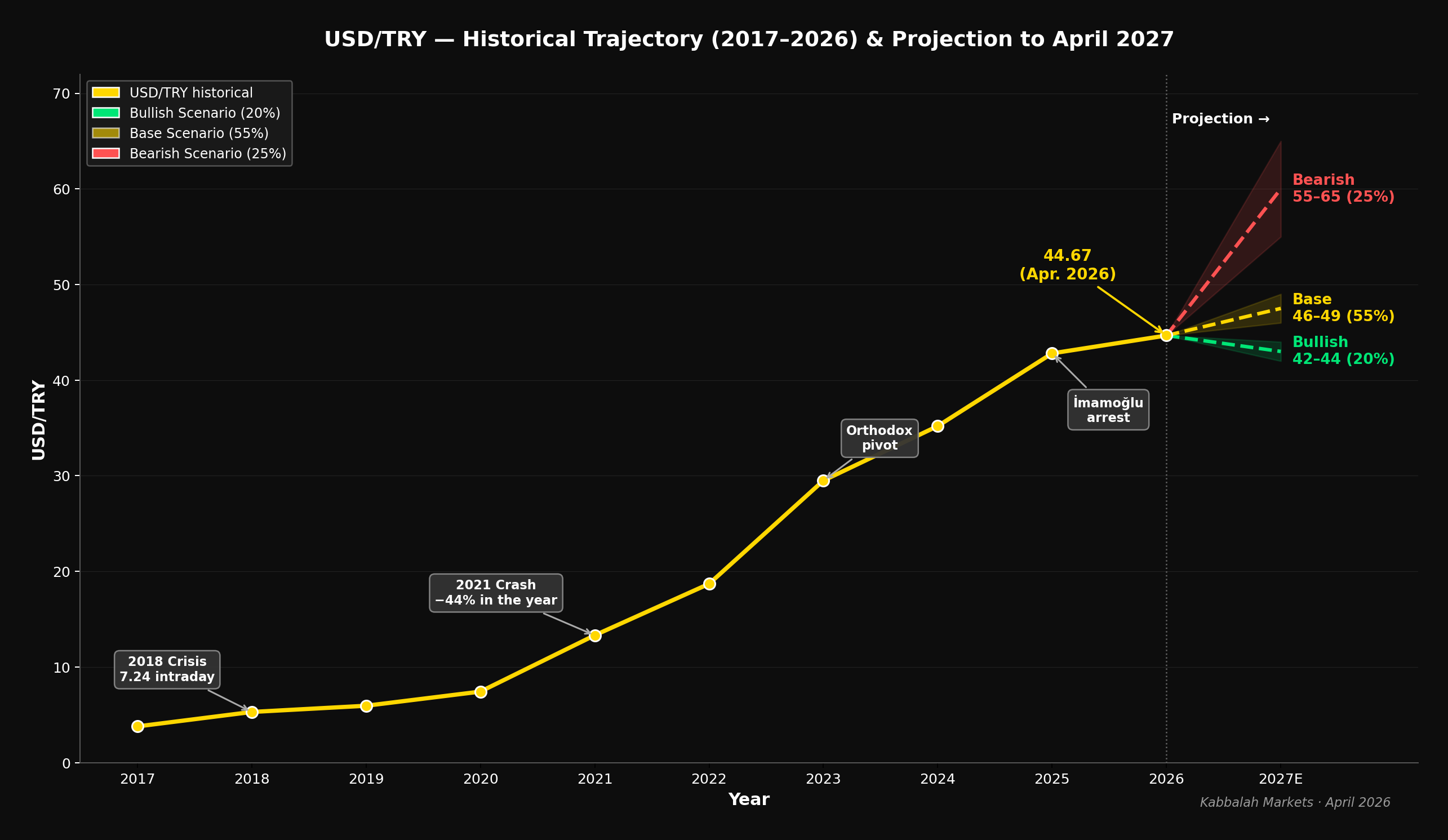

IV. USD/TRY Analysis — 12-Month Projection

Current rate and context

USD/TRY reached 44.67 on April 10-11, 2026 — the all-time high up to that date. The lira has depreciated 17.8% over the past 12 months (from ~37.91 a year ago), and 3.96% so far in 2026. The TCMB has maintained a managed crawling peg — the lira depreciates approximately 20-25% annually, consistent with the inflation differential, with interventions to moderate volatility.

Historical trajectory

| Year | USD/TRY (close) | Main event |

|---|---|---|

| 2017 | ~3.77 | Expanding economy |

| 2018 | ~5.28 (intraday max. 7.24) | Currency crisis: US sanctions, Brunson case |

| 2019 | ~5.95 | Partial recovery |

| 2020 | ~7.41 | COVID-19; TCMB burned ~$93 billion in reserves |

| 2021 | ~13.32 | 2021 crash: -44% lira; rate cuts amid inflation |

| 2022 | ~18.70 | 80% inflation; KKM implementation |

| 2023 | ~29.51 | Post-elections; pivot toward orthodoxy; rates 8.5% → 42.5% |

| 2024 | ~35.20 | Rates at 50%; inflation fell from 75% to 44% |

| 2025 | ~42.85 | Cutting cycle; İmamoğlu crisis (March) |

| 2026 (Apr. 10) | ~44.67 | Pause due to geopolitical shock |

Sources: Wikipedia – Turkish economic crisis) | Exchange Rates UK | FreeCurrencyRates

Structural weakness factors

Inflation differential. With Turkish inflation at ~31% versus ~2.5% in the US, the structural differential of ~28 percentage points presupposes a similar nominal depreciation to maintain the real exchange rate. Even in the best scenario (Turkish inflation at 16% by year-end), the differential remains at ~13 points — implying annual depreciation of that magnitude just to maintain purchasing power parity.

Current account. The deficit on a rolling 12-month basis reached $32.9 billion (2.2% of GDP) in January 2026. ING projects the deficit at $45 billion (2.9% of GDP) for 2026 under the impact of the energy shock — practically doubling the 2024 level.

Oil shock. Brent at $118/barrel implies $22-24 billion in additional annualized energy spending. Turkey's energy bill already exceeded $65 billion in 2025 at moderate prices. The government uses a sliding scale tariff system that absorbs ~75% of the inflationary impact but carries a significant fiscal cost.

Political risk. The judicial process against İmamoğlu pushed Turkey's sovereign CDS above 300 basis points in March 2026 (9-month high). The accumulated carry trade is around $40-55 billion — the highest level in EEMEA emerging markets — and is highly sensitive to political news.

Carry trade dynamics

The lira was designated in February 2026 as the favorite carry trade in EEMEA by Bank of America, with estimated potential returns of ~10%. Goldman Sachs recommended long TRY positions with a target return of 7.5%. The total accumulated carry was 77% higher than the previous year. However, in March 2026 approximately $15 billion was unwound in response to the regional conflict — with 3-month forward rates reaching 47.3% at the peak of stress. The high leverage of the trade is its greatest fragility: it is the most compressed in emerging markets, generating violent reversals at any political or geopolitical shock.

Bank projections

| Institution | USD/TRY end-2026 | 2026E Inflation | Notes |

|---|---|---|---|

| Goldman Sachs | ~45.0 | — | Carry trade; moderate depreciation |

| JPMorgan | ~48.0 | ~32% | Policy risks; end-2026 rate ~30.5% |

| Morgan Stanley | ~44.0 | — | TRY among the strongest in CEEMEA |

| Deutsche Bank | ~52.0 | ~23.8% | Bearish; carry weakening |

| ING | ~51.0 | ~22% | Controlled depreciation; widened CA deficit |

| S&P Global | ~47.0 | 15-19% | Cautious; structural reforms needed |

| Commerzbank | ~44.0 | — | Q1 target nearly achieved |

| LongForecast | ~52.0 | — | Average monthly depreciation 1.9% |

Consensus range end-2026: 44–52; median ~47–48.

Sources: Capital.com Forecast USD/TRY | NAGA Forecast | Exchange Rates UK

Scenarios over 12 months (April 2026 → April 2027)

| Scenario | USD/TRY at 12 months | TCMB rate end-2026 | Inflation end-2026 | Probability |

|---|---|---|---|---|

| Bullish (Stabilization) | 42–44 | 28–30% | 15–18% | 20% |

| Base (Controlled depreciation) | 46–49 | 29–31% | 20–25% | 55% |

| Bearish (Further collapse) | 55–65 | 35%+ | 30%+ | 25% |

Bullish scenario (20%): Requires the Middle East ceasefire to consolidate, Brent to return to $60-65, inflation to surprise to the downside (~15-17%), and the carry trade to reactivate forcefully. The room for real appreciation is limited even in this case — with a residual differential of ~13 percentage points, the lira would still need to depreciate at least that amount to maintain the REER.

Base scenario (55%): The rate reaches ~29-31% by year-end, inflation converges toward 20-24% (above the official 16% target), oil moderates to $70-80/barrel, and the lira depreciates at the historical rate of the inflation differential (~15-18% annually). Tourism maintains revenues around $60 billion, supporting the services balance.

Bearish scenario (25%): The regional conflict escalates, Brent sustains above $100/barrel, inflation re-accelerates above 30-35%, the TCMB is forced to cut rates rapidly under political pressure, and the carry trade experiences a massive reversal of $40-50 billion. This scenario has historical precedent: the lira fell 44% in 2021 and nearly 45% in 2018.

V. Kabbalistic Reading

Master gematria table

| Value | Hebrew | Transliteration | Meaning / Connection |

|---|---|---|---|

| 18 | חי | Chai | Life — fundamental unit of the cycle |

| 38 | גלה | Galah | Exile / Revelation — USD/TRY level 2025 |

| 51 | אדום | Edom | Rome → Byzantium → Western Turkey |

| 72 | חסד | Chesed | Kindness — the counterforce of Gevurah |

| 137 | קבלה | Kabbalah | The reception |

| 144 | ביזנטיון | Byzantion | 144 = 12² (12 tribes squared) |

| 168 | איסטנבול | Istanbul | 168 = 7 × 24 = one complete week |

| 216 | גבורה | Gevurah | The Sefirah of Edom / Turkey |

| 240 | ליר | Lir / Lira | = רם (Ram / Exalted) |

| 245 | לירה | Lirah | = 5 × 49 (5 Jubilees) |

| 288 | חסד + גבורה | Chesed + Gevurah | The 288 fallen sparks (Nitzotzot) |

| 354 | בוספור | Bosphorus | = lunar year (354 days) |

| 376 | עשו | Esav / Esau | = שלום (Shalom / Peace) — identical |

| 376 | שלום | Shalom | = עשו (Esau) — the peace of exile |

| 416 | קושטא | Kushta / Constantinople | = קושי (Koshi / Difficulty) |

| 451 | ישמעאל | Yishmael | Ishmael — 502 with Edom = Haman/Mordecai |

| 496 | מלכות | Malkhut | Kingdom — the physical plane, material Turkey |

| 502 | אדום + ישמעאל | Edom + Ishmael | = "Cursed Haman" = "Blessed Mordecai" |

| 570 | תקע | Tekiah | Shofar blast — 1453 + 570 = 2023 |

| 641 | תורכיה | Turkiyah | Turkey — prime number |

Turkiyah = 641: prime sovereignty

The standard gematria of תורכיה (Turkey) is 641. That number has a singular mathematical property: it is a prime number — indivisible, non-factorable, divisible only by itself and by unity. This kabbalistic condition is not an accident: Turkey operates with a singular logic that resists conventional analysis. It cannot be broken down into smaller parts because its spiritual function is to be indivisible.

The digital root of 641 is 2 (6+4+1=11; 1+1=2) — the value of ב (Bet), the first letter of the Torah, the letter of Bereshit: "In the beginning." Turkey vibrates at the frequency of beginning, of the threshold, of the vessel that has not yet been completely filled.

Lira = Ram = 240: the exalted in exile

ליר (Lira, short form) sums to 240 in standard gematria. That same value belongs to רם (Ram) — exalted, elevated. The Turkish Lira carries inscribed in its numerical structure the code of elevation. What the market perceives as a currency in continuous collapse is, from the Kabbalah's perspective, an exalted power undergoing its process of Tzimtzum — the contraction that precedes expansion.

The full form לירה sums to 245 = 5 × 49. Five times the Jubilee. Forty-nine is the number of the Jubilee year (year 50, when slaves are freed and lands returned). The Lira carries in its full name the promise of liberation, multiplied by the divine breath (5 = ה).

The 38 = Galah: the spiritual thermometer

When USD/TRY passed through 38, the currency market was operating at the frequency of גלה (Galah) — a word with two simultaneous and inseparable meanings in Hebrew:

1. Exile (גלות / Galut): being taken to a foreign land, the concealment of light 2. Revelation (גילוי / Gilui): to uncover, reveal, make the hidden visible

The same root, the same letters, the same number. The exchange rate is not only a macroeconomic figure: it is a barometer of the spiritual state of the relationship between Turkey and its potential. The Ari (Isaac Luria, the greatest post-Talmudic kabbalist) died at age 38 — exactly Galah. His death was the condition for the transmission of all Lurianic Kabbalah. The deepest exile contained the highest revelation.

"The exchange rate is the thermometer of Turkey's exile and revelation. The 38 encodes both the nadir and the threshold."

The chain Esau → Edom → Rome → Byzantium → Ottoman → Turkey

In Jewish and kabbalistic tradition, the nation of Esau (Edom, אדום = 51) undergoes a succession of historical incarnations identified by the sages:

ESAU → EDOM → ROME → BYZANTIUM/CONSTANTINOPLE → OTTOMANS → MODERN TURKEY

The prophet Daniel (ch. 2) describes four empires as materials: Gold (Babylon), Silver (Persia), Bronze (Greece) and Iron + Clay (the fourth divided kingdom). The Midrash Tanchuma and Rav Sa'adia Gaon identified the fourth kingdom as Edom — and Rav Sa'adia Gaon elaborated that it is divided in two: Edom (iron = military power) and Ishmael (clay = numerical ubiquity).

The genealogical connection is precise: Esau married Hittite women — the Hittites inhabited Anatolia (Asia Minor = present-day Turkey). The Khazars called the Byzantine Emperor in Constantinople "the King of Edom," directly confirming the identification. Ibn Ezra (12th c.) writes in his commentary on Isaiah 63:1: "This prophecy contains the decree against Edom, that is, against the Empire of Rome and Constantinople."

The most revealing kabbalistic equivalence: עשו (Esau) = שלום (Shalom) = 376. The "peace" offered by the world of Edom/Esau has exactly the same gematric weight as his name. The "Peace of Esau" is tautological: it comes from the same source as the restriction.

Gevurah: Turkey's Sefirah

In Kabbalah, the Kings of Edom (Genesis 36:31-43) — eight kings who reigned before there was a king in Israel — are the broken vessels of the World of Tohu. Eight vessels that could not contain the light and shattered. The sum of that rupture is precisely the field of Gevurah (גבורה = 216) — the fifth Sefirah, the left arm of judgment, restriction without mitigation by mercy.

But Gevurah is not evil: it is the function that makes form possible. Without Gevurah, Chesed overflows without limit and destroys what it touches. The Gevurah of Turkey/Edom creates the vessel — the receptacle — where light can be deposited without being consumed.

The fundamental equation of the shattering of the vessels is:

The 288 sparks that dispersed when the vessels shattered in the Shevirat HaKelim are the exact sum of the two opposing attributes. Turkey operates in the field where these sparks await elevation — and history shows that in this field the greatest revelations flourish.

The Bosphorus as ontological frontier

בוספור (Bosphorus) = 354 = days in the lunar year. This equivalence is extraordinary and precise: the strait dividing Europe from Asia, West from East, Edom from Ishmael, carries in its Hebrew name the same value as the complete lunar year — the time of the feminine-receptive cycle, the time of the Shekhinah in a state of division awaiting reunification.

To the west of the Bosphorus: the European, Christian heritage, Edom (Byzantium, Rome). To the east of the Bosphorus: the Asian, Islamic heritage, Ishmael (Central Asia, Arabia). The Bosphorus is not only a geographical border — it is the ontological axis between the two eschatological forces of the present time. The Ottoman Empire absorbed Christian Byzantium and governed as an Islamic power, becoming the living embodiment of both traditions simultaneously — which makes Turkey the kabbalistcally most complex nation in the world.

There also exists a Jewish tradition that identifies the legendary River Sambatyon (where the ten lost tribes were exiled) with the Bosphorus. If this identification is correct, the final reunification of Israel will include the reverse crossing — back through the Bosphorus. The strait is the border between exile and return.

The Zohar prophecy (Va'era, folio 32a)

The Zohar contains one of the most explicit prophecies about the end times in relation to Ishmael and Edom. In the portion of Va'era, folio 32a:

"In the future, the children of Ishmael will stir up great wars in the world. The children of Edom will gather against them and wage three battles: one at sea, one on land, and one near Jerusalem. And they will dominate one another, but the Holy Land will not be handed over to the children of Edom..."

— Zohar, Shemot 32a

For Kabbalah Markets: "the children of Edom" = Western civilization (Rome → Europe → the West → USA). "The children of Ishmael" = the Arab-Islamic world. The US-Israel-Iran war of February 2026 — with Turkey as the neutral mediator at the only point of contact between both sides — carries textual resonances with this prophecy that deserve rigorous attention. The "nation from the ends of the earth" that rises against Rome is cited by multiple commentators as a possible reference to China or Russia.

The fifth and final Jewish exile is, according to Rav Chaim Vital, the Exile of Ishmael — "harder than any of the previous ones" because Ishmael "is a son of Abraham and has the merit of the patriarchs." The Ottoman Empire was literally that exile — and under it Lurianic Kabbalah flourished. The spiritual paradox is perfect: the hardest exile created the conditions for the highest revelation.

Sabbatai Zevi and the kabbalistic DNA of the Turkish Republic

The most dramatic event in post-Zoharic Kabbalah occurred in Istanbul. In 1666, Sabbatai Zevi — the most celebrated messianic claimant in Jewish history — was imprisoned by the Ottoman sultan and, faced with the dilemma of conversion or death, converted to Islam. His radical followers, the Dönmeh (converts in Turkish), practiced a hybrid Islamic-Jewish Kabbalah in secret for centuries. According to the Encyclopaedia Britannica, the Dönmeh maintained this practice into the 20th century. Historians have documented that many Dönmeh played central roles in the Young Turks Movement and in the founding of the Turkish Republic in 1923.

The line is direct: Kabbalah of Safed (16th c.) → Sabbatai Zevi (1666) → The Dönmeh → The Turkish Republic (1923). The modern nation of Turkey has kabbalistic DNA literally inscribed in its founders.

1453: the year of the threshold

The fall of Constantinople in 1453 marked the end of the Byzantine/Edom Empire and the beginning of the Ottoman/Ishmael era. For the Jewish community this meant: the end of Christian-Edomite persecution in that region, the opening of the Ottoman period of relative tolerance, and the creation of the space for the wave of Sephardic refugees of 1492 — who would bring the Kabbalah to Safed. The harshness of the transition created the vessel for the greatest spiritual revelation of the post-Talmudic era.

VI. Synthesis: Where Is the Lira Heading?

The four-dimensional map

The comprehensive analysis of Turkey in April 2026 reveals a system of forces that only makes full sense when all four dimensions are read together:

The economic fundamentals point to structural depreciation that continues at the rate of the inflation differential (~20-25% annually). The base scenario of investment banks (USD/TRY 46-49 for April 2027) is consistent with this mechanic. The current account is widening, net reserves have deteriorated, and the energy shock has interrupted the disinflation cycle. There is no abrupt reversal on the near horizon from this reading.

The geopolitical positioning is improving, not deteriorating. Turkey hosts the NATO summit, reactivated the Kirkuk-Ceyhan pipeline, is the only point of contact between Washington and Tehran in the most serious regional conflict in decades, has achieved its greatest strategic victory in Syria, and consolidates an emerging military alliance with Pakistan. Each of these moves increases Turkey's strategic indispensability — which is, over the long term, the Lira's most solid asset.

The kabbalistic reading adds the dimension that conventional analysis omits: the process has direction and purpose, it is not chaos. The Lira = Ram = Exalted. Its fall is Tzimtzum — the necessary contraction so that the vessel can receive more light than it could contain without that prior process of formation. The exchange rate at level 38 = Galah — the exact point where exile and revelation are indistinguishable.

The cycles and the 2031 horizon

The structure of kabbalistic cycles around Turkey converges toward identifiable inflection points:

1453 + 570 (Tekiah) = 2023: the centenary of the Republic coincided with exactly one Tekiah (570 = תקע, the long shofar blast that proclaims the Jubilee) since the fall of Constantinople. The centenary sounded like a shofar of 570 years duration.

Chai cycles (18) from 1923: the fifth cycle (5 × 18 = 90 years) arrived in 2013 — the year of the Arab Spring and the first serious tensions between Israel and Turkey. The sixth cycle (6 × 18 = 108 years) points to 2031 — and 108 = קח (Kach / "Take, Receive"), the year of Kabalat HaMalkhut — the "Taking of the Kingdom."

The year 103 = 2026: 103 is a prime number (like Turkey itself). Its digital root is 4 = ד (Dalet) = door, threshold. Words with gematria 103 include מחנה (Machaneh = camp) and נחמה (Nechamah = consolation). The year 2026 is the year of the camp before the final movement — a year of positioning, not of arrival.

5786 = 786 = Bismillah: the Hebrew year 5786 has a value without the millennial prefix of 786 — exactly the Arabic numerical value (Abjad) of the Bismillah (بِسْمِ اللَّهِ الرَّحْمَٰنِ الرَّحِيمِ). The Hebrew year and the Islamic opening formula share the same number. 2026 is the year where the Hebrew and Arabic alphabets converge at the same frequency — the year of the encounter between traditions.

The integrated projection

| Dimension | Signal for USD/TRY | Horizon |

|---|---|---|

| Economic fundamentals | Continued depreciation ~20%/year | 12-24 months |

| Inflation differential | Structural pressure of ~28pp | Permanent until convergence |

| Geopolitical position | Improves long-term narrative | 3-5 years |

| Kabbalistic cycle (Chai) | Contraction (Gevurah) until 2031 | 5 years |

| Gematria: Lira = Ram (240) | The elevation is encoded | Latent |

| Galah (38): already transited | The nadir of exile was 2025 | Past |

| Tekiah sounded (2023) | The shofar already called | Active process |

| 2031: 6th Chai = Kach | Next major inflection point | 2031 |

Integrated base scenario: USD/TRY 46-49 for April 2027, consistent with banking consensus and fundamentals. But the kabbalistic reading reframes what this means: this is not a disorderly collapse but a Gevurah contraction — restrictive, dense, purposeful. The vessel is being formed. The five years until the 6th Chai cycle (2031) are the period of Machaneh — the camp where position is consolidated before the decisive movement.

The investor who understands that Gevurah precedes the expansion of Chesed does not exit the trade out of fear — exits when the process is complete. The Lira at its current level is not a broken asset: it is an asset in the process of forming the vessel.

Table of Cycles and Key Dates

| Year | Event | Interval | Kabbalistic frequency |

|---|---|---|---|

| 1453 | Fall of Constantinople — end of Edom-Byzantium | — | — |

| 1492 | Expulsion from Spain; Jews to the Ottoman Empire | +39 years | — |

| 1534 | Birth of the Ari under Ottoman rule | +42 years | — |

| 1570 | The Ari arrives in Safed | +36 years | — |

| 1572 | Death of the Ari at age 38 = גלה | +2 years | Galah (38) |

| 1666 | Sabbatai Zevi in Istanbul — the Dönmeh | +94 years | 1+6+6+6 = 19 = חוה |

| 1923 | Turkish Republic — founders with kabbalistic DNA | +257 years | New cycle |

| 2023 | Centenary — 1453+570=2023 | +100 years | Tekiah (570) |

| 2026 | Year 103 = Machaneh = 5786 = Bismillah | +3 years | Door/Threshold |

| 2031 | 6th Chai from 1923 = Kach = "Receive" | +5 years | Next inflection |

Final Words from Kabbalah Markets

Markets do not lie — they distort. What appears to be a collapse of the Turkish Lira is, from the angle this analysis illuminates, a process of formation: the Tzimtzum that creates the space where something greater can enter. Turkey is not a story of economic failure with a geopolitical veneer: it is a nation that carries in its gematria (641 = first prime number of its range), in its currency (240 = Ram = Exalted), in its historic capital (416 = Kushta = Truth and Difficulty simultaneously), and in its most sacred strait (354 = the complete lunar year), the entire architecture of a major transition in progress.

Gevurah is not Turkey's destiny — it is the antechamber. The vessel formed under restriction has greater capacity than the one built under abundance. The sixth Chai cycle (2031) is five years away. Those five years are not years of passive waiting: they are the Machaneh — the camp where those who understand where the process is heading position themselves.

The Lira will fall before it rises. USD/TRY will reach 46-49 in the base scenario before finding its structural inflection point. Those who buy fear sell at the nadir. Those who buy understanding — Binah, the Sefirah of deep comprehension — arrive first.

The shofar of Tekiah already sounded in 2023. We are in the year of the Machaneh. The next sound is the Shevarim — the breaking. And after the breaking, the Tekiah Gedolah.

Kabbalah Markets · Turkey Comprehensive Analysis · April 2026

Primary sources: TCMB | IMF Art. IV 2025 | BDDK | World Bank | BBVA Research | BNP Paribas | ING Think | Atlantic Council | FDD | Carnegie Endowment | PA Turkey | Trading Economics | GalEinai | Zohar Shemot 32a via Jerusalem Post | Encyclopedia Britannica – Dönmeh | World Mizrachi | Torah.org – Kushta

VIX. 18.33. Monthly candle opened at 24.30, high of 28.00, collapsed −27.38% to here. The monthly low: 17.40.

The lifetime median VIX since 1990 is 17.84. The lifetime mean is 19.71. The middle 50% of all readings sits between 14.04 and 23.98. At 18.33, volatility is exactly at the median — the historical fulcrum.

In Hebrew, 18 = Chai (חי) = Life. The VIX is sitting on the Chai level.

March spike: 17.93 → 31.05 in 22 sessions (+73%). Then 31 → 18 in seven trading days. Classic mean reversion. Term structure back in contango — fear fully unwound. Put/call ratio swung from 1.11 (Mar 31, panic) to 0.29 (Apr 14, complacency). VVIX at 97.65 — vol-of-vol contained.

Hebrew distinguishes two types of fear. Pachad (פחד) — dread, the paralytic terror that consumes. And Yirah (יראה) — awe, the fear that elevates. Yirah = Gevurah (גבורה) = 216. At 31, the VIX was Pachad. At 18, it has returned to Yirah — measured awareness, not panic.

Two gematria levels to watch. Below: 13 = Ahavah (אהבה, Love) = Echad (אחד, Unity). The complacency floor. 52-week low was 13.38. When love fills the market, buy protection. Above: 26 = the Tetragrammaton (יהוה). VIX tested 25.78 on April 7. The Name level held. A break above 26 signals Gevurah taking command.

Pachad paralyzes. Yirah elevates. Know which fear you hold.